More Stories

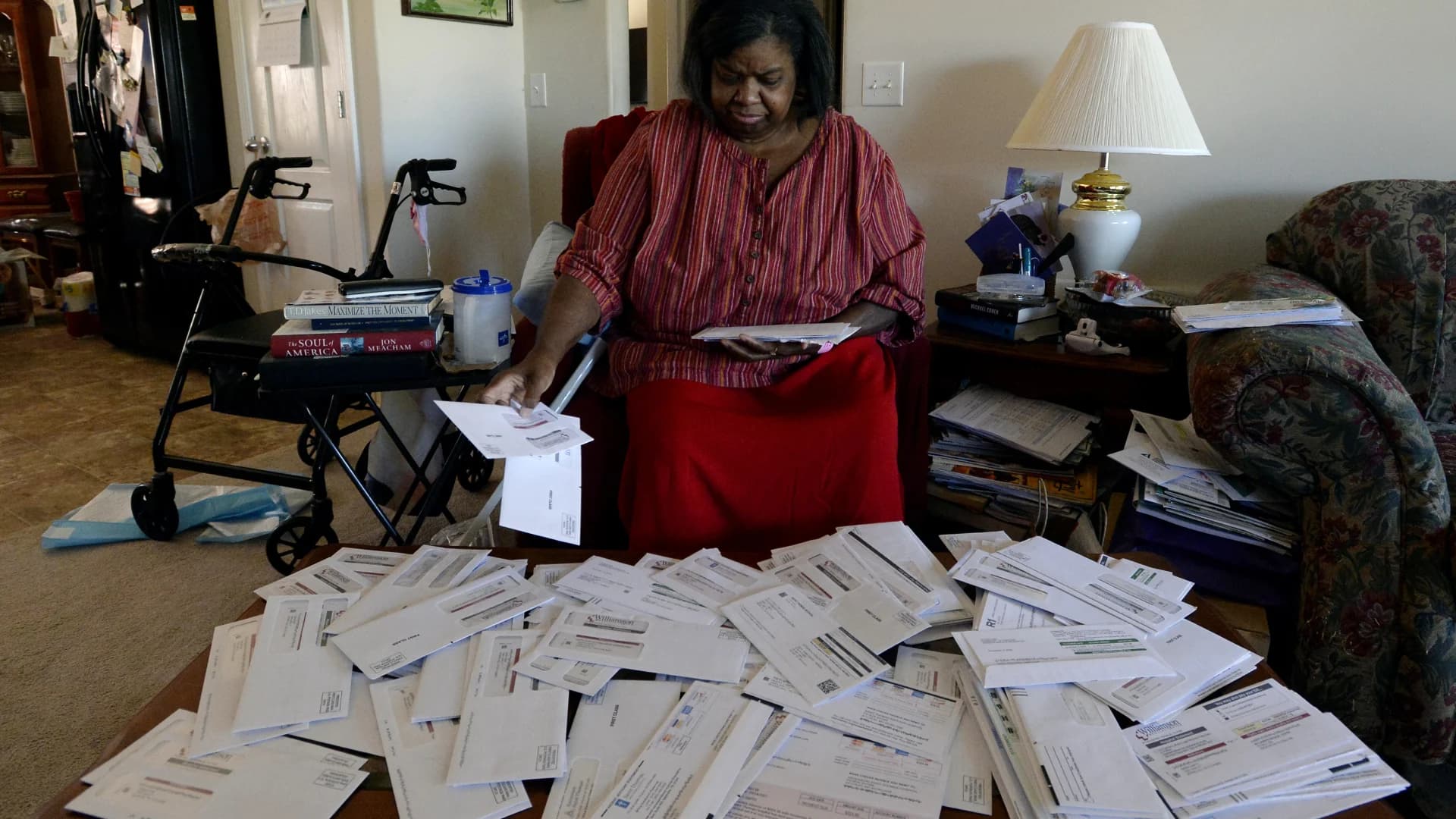

When she was 19, writer Emily Maloney found herself facing about $50,000 in medical debt after hospital treatment for a mental health crisis. The debt followed her throughout her twenties, hurting her credit and leading to stressful calls from collection agencies.

Her experience is all too common: The Consumer Financial Protection Bureau reports that about 1 in 5 U.S. households carries medical debt. People with medical debt are more likely to face anxiety, stress or depression and avoid filling prescriptions because of the cost.

The risk of “medical debt looms over every consumer and impacts their lives,” says John McNamara, assistant director of consumer credit, payments and deposits markets at the CFPB. He adds that recent changes to the way medical debt is reported by credit bureaus should help consumers: Paid medical debts will no longer show up on credit reports and no new medical debt will show up until 12 months have passed (up from six months). In addition, in the first half of next year, the credit bureaus will stop reporting unpaid medical debts under $500.

Eventually, Maloney’s debt was resolved through a combination of a helpful customer service representative and exceeding her state’s statute of limitations. She wrote a book, “Cost of Living,” based on her experiences. She wants to assure others facing medical debt that they can take steps to reduce it.

“It takes time, but you can appeal the insurance company’s decision or ask (the provider) for a discount, so it’s worth a shot,” she says.

In other words, consumers might have more power than they think. Here are some ways to exercise that power over your medical debt.

REVIEW YOUR BILL CLOSELY

It can be tempting to shove a large bill into the trash in frustration. But Dan Weissmann, creator of “An Arm and a Leg,” a podcast about the cost of health care, instead recommends checking closely for errors made by the care provider or insurance company.

“It’s an unfair amount of homework for us to do, because if you find an error, then you have to complain and invest your time, but some medical bills have errors,” he says.

Weissmann says it’s also worth checking your rights under the No Surprises Act, which went into effect in January 2022 and protects consumers from some types of unexpected medical bills.

ASK YOUR PROVIDER FOR ASSISTANCE

Many hospitals offer financial assistance to those who meet income thresholds. “If you get an amount you weren’t expecting, call the hospital and say, ‘Am I eligible for a discount? What is your policy on financial assistance?’” says Richard Gundling, vice president at the Healthcare Financial Management Association , an association of financial executives in the health care industry.

Hospitals often have “charity care” policies to grant a lower price or even forgive the debt altogether, but consumers may have to be aggressive in asking for them. Eligibility for the programs varies by state and hospital, but nonprofit hospitals are required to have financial assistance policies. Hospitals may also offer payment plans, so you have more time to pay.

Hospitals can also connect you with financing options such as personal loans and medical credit cards, which can be helpful but also pose risks. The CFPB’s McNamara warns that credit cards, for example, can accrue additional interest charges.

BE PERSISTENT AND ENLIST SUPPORT

Lorraine Coughlin, president of LMC Medical Claims Management in West Palm Beach, Florida, helps people work out medical bills with insurance companies for a living. She says the number one strategy is persistence.

“You have to make the phone call and ask questions. Don’t just make payments if you get a surprise bill,” she says. Sometimes it might take an hour or more, but making that call can save you thousands of dollars, she says.

Medical billing advocates like Coughlin can do that work for you, but they typically charge a fee and a percentage of any savings. McNamara warns there are predators who call themselves billing or consumer advocates but in reality, they could take your money without providing any real assistance. He recommends doing some research before sharing any personal information or paying upfront fees.

If you are struggling to get satisfactory answers from your insurance company and are employed, Gundling suggests asking your company’s employee benefits contact for help. “They can be your advocate,” he says.

GET READY FOR THE NEXT MEDICAL BILL

The ideal time to work on handling medical debt is before you have it, Gundling says. With the rise of high-deductible health insurance plans, even people with insurance will increasingly face pricey bills, which makes an emergency fund even more important.

“If you know you have a plan with a large deductible, have the cash in the bank,” he says.

You could try setting money aside through automated deposits into a high-yield savings account or taking advantage of a health care flexible savings account if your employer offers one.

Similarly, Gundling suggests asking questions about what your insurance covers and which providers are in-network before seeking care whenever possible.

The bottom line is that attacking, not ignoring, medical debt can be your best hope of eventually putting it behind you as Maloney did.

By KIMBERLY PALMER of NerdWallet

More from News 12

1:19

Shots fired near The Adlai E. Stevenson Campus

2:02

Early rain ahead of a decent spring weekend for The Bronx

0:21

Person wanted in connection to teen shooting in Soundview

1:35

NYPD: 2 officers hospitalized after traffic stop turns into car chase, crash

0:26

Accused chain snatcher in Mott Haven is at large, police say

0:28